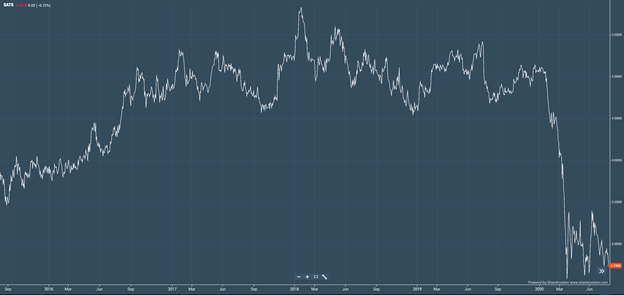

A lot of readers have asked me for my view on SATS.

With a chart like the below, it’s not that hard to see why too. You’re getting this stock at close to 50% cheaper than where it was in Jan 2020, just 6 months ago. That’s a 100% upside if it ever goes back there.

Source: ShareInvestor WebPro

Lots to cover today, so let’s jump right into it.

Note: The research for this article, and most of the charts here, are sourced from ShareInvestor Webpro. It’s a great way to quickly perform research on Singapore stocks, far more comprehensive and flexible than other options like Yahoo Finance.

You can learn more in my review on ShareInvestor Webpro here.

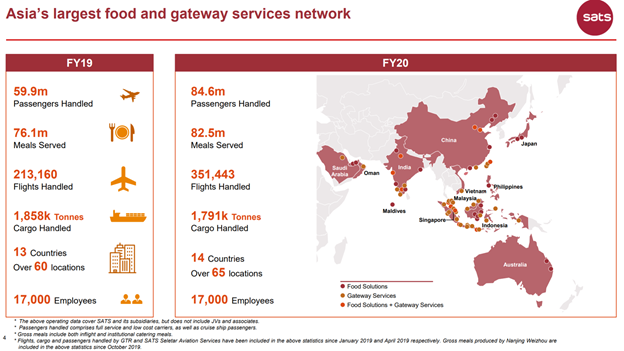

Basics: What is SATS?

Very simply, SATS is Asia’s leading provider of (1) Gateway Services and (2) Food Solutions

Gateway Services are things like Cargo handling and Passenger baggage handling.

Food Solutions are things like Flight Catering, Food catering or Singapore Food Industries (SFI for the guys out there – basically our cookhouse food

Basically, they provide baggage and cargo handling services for airlines, and they provide flight catering to airlines. The more airlines that fly, the more money they make. The less airlines they fly, the less money they make.

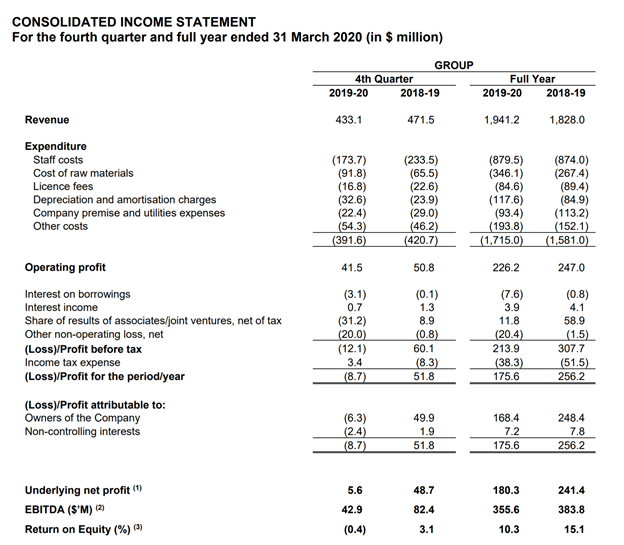

SATS P&L Pre-COVID

Source: ShareInvestor WebPro

The Income Statement Pre-COVID is set out above, and to be honest, I can really see why this stock was trading at $5 pre-COVID.

It makes good profits, comfortable double digit margins, and operates in a monopoly industry with big barriers of entry. And pays a nice 4% dividend yield.

Problem is – COVID19 has been an absolute gamechanger.

Post-COVID, none of the pre-COVID numbers make much sense anymore. We need to reason from base principles, and think about how the business will perform going forward.

Impact from COVID-19

A big chunk of SATS earnings (approx. 85%) is tied to the aviation industry. With the aviation industry grounded, earnings are going to be impacted massively.

Sure, some of the cargo airline services will continue to persist, but almost all of the international air travel is just gone.

We looked at Comfort Delgro last week, which is basically a play on domestic travel. I’m more optimistic on domestic travel, because I think that when Singapore manages to control COVID-19, life can gradually resume, at least within our shores. This will drive the take up of domestic transport.

International travel though, is a whole different ballgame.

Singapore is an island, without a large domestic market to rely on. We don’t have the big domestic blocs of travel that the US, China or EU can rely on. Airlines in those countries are at least better off, because at some point people still need to travel within the country.

With Singapore though, all travel is just purely international. You can’t get on an airplane and fly from Changi to Jurong, it has to be Changi to London Heathrow, or Beijing Daxing.

That leaves us at the mercy of other countries.

Just because Singapore wants to fly to London, doesn’t necessarily mean London will agree. It will have to depend on (1) how well Singapore controls COVID-19, in the eyes of the world, (2) how well that country controls COVID-19, in the eyes of Singapore, and (3) how good are the relations between the countries, to work out travel arrangements.

What is SATS doing?

This is what SATS had to say about COVID-19

However, there is no doubt that the way we fly will change, so SATS is working closely with our customers to reimagine air travel in a post-pandemic world. Even as we work to ensure operational continuity for today’s disrupted aviation industry, we are developing new offerings for a low-touch future, incorporating digital solutions, new food technology and sustainable packaging.

Our investments in technology and digitalisation have enabled us to respond with agility and flexibility to the needs of new customers and the community during this crisis. In particular, we expect our food trading and distribution business to continue to grow, as we build our non-aviation food revenues.

Basically, they know that COVID-19 has been a game changer. They have 2 options:

(1) Do nothing, and wait for COVID-19 to go away and earnings to recover.

(2) Try to diversify away from air-travel, while preparing for a post-COVID world.

I don’t think any management can justify going with (1), so they went for (2).

Diversifying the income stream

A DBS Report breaks it down nicely:

Non-aviation revenues made up 17% of group revenues in FY20. SATS continues to leverage on its kitchens to provide more institutional catering through supply contracts with corporate clients and events.

It has a 21-year catering and food and beverage (F&B) services contract with the Singapore Sports Hub from 2014, through a 70/30 JV with global hospitality company Delaware North Companies.

SATS also has a Kunshan central kitchen which supplies food products to customers in fast casual restaurants as well as the aviation sector. In addition, Gateway revenue traction that is building up led by the Marina Bay Cruise Centre will also help to diversify revenue streams from the aviation sector.

So SATS is definitely trying. They’re trying to diversify their income stream away from aviation.

As at FY2020 though, it still only comprised 17% of revenue.

The big question then – Will SATS succeed?

My take, is that they will succeed to a certain extent. They will find ways to earn money from food catering, from doing cargo related work, from packing food etc. But will this be enough to offset the decline in the aviation business? No way.

Is liquidity / solvency a concern?

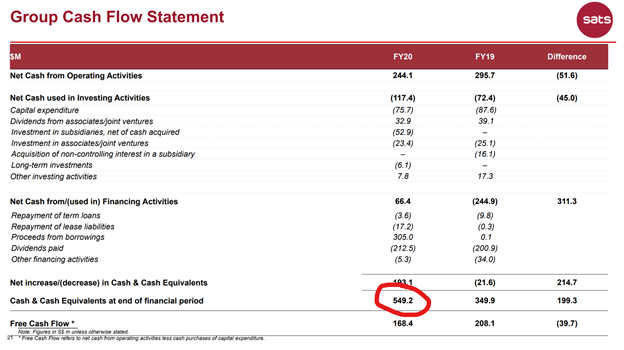

The business for SATS is so bad that we need to check on liquidity and solvency.

Basically, SATS spends about $391 million a quarter.

In a good quarter, they pull in more than $400 million a quarter, turning a nice profit.

How much will revenue drop post-COVID though?

We only have the Q1 (Jan to March) results so far, which are not helpful because the global situation wasn’t that bad then yet.

Let’s conservatively assume a 50% fall in revenue. Revenue drops to $235 million per quarter.

With $391 million in costs, that’s a $156 million cash burn a quarter.

SATS drew down on the bank loans earlier this year, anticipating a cash crunch. So they now have $549 million cash on hand.

At this rate, the cash only lasts 3.5 quarters, or 10 months.

Of course, these are just very rough numbers.

But the math is clear.

SATS current trajectory is not sustainable. There are only 2 options here: (1) Cut their expenditure, or (2) raise additional financing.

Cutting Expenditure

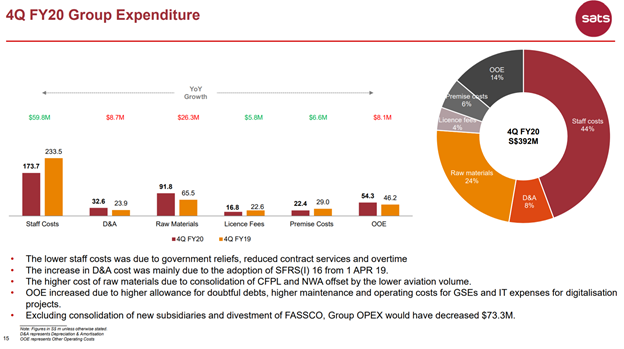

The 2 biggest components are staff costs (44%), and raw materials (24%), ie. The cost of food.

SATS is a Temasek linked company, so they probably cannot retrench staff in a big way.

The government is paying for salaries though, under the Job Support Scheme. This covers 75% of salaries up to $4600, for a period of 9 months. This has helped cut staff costs from $233.5 million per quarter to $173.7 per quarter.

This won’t last forever though, it will expiry towards the end of the year.

Raw materials cost will also drop, because if they don’t need to handle flight catering, they don’t need to buy the food anymore.

To smooth it all out, let’s just assume SATS manages a 10% cut in expenditure from the 4Q numbers (which already include the wage subsidies).

That takes cash burn a quarter to $117 million, which means their current cash lasts 14 months.

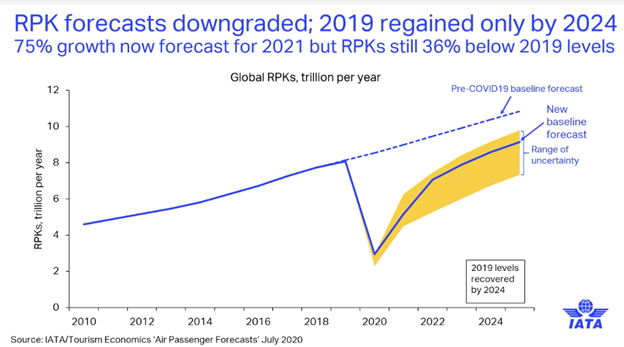

When will international airtravel recover?

14 months will take us to middle of 2021. Will international aviation recover by then?

It’s tricky.

Let’s assume optimistically we get a vaccine in early 2021. We start ramping up production, in first half of 2021, but realistically, only the healthcare and high risk workers will get the first doses.

For the mass population in developed countries, we’re probably looking more realistically at late 2021.

For emerging markets to get it, we’re probably looking at 2022.

Boeing came out in their latest earnings call to say that they don’t see global air travel recovering to pre-COVID levels for 3 years. That will take us into 2022, in line with this estimate.

IATA is even more pessimistic. They expect recovery only in 2024 (to pre-COVID levels).

Raise additional financing

SATS balance sheet does look a bit precarious in this context.

I wouldn’t rule out the possibility of additional fundraising here.

SATS currently sits on a 38% gearing ratio, so there’s room for additional bank borrowings.

The other possibility of course, will be equity fund raising, something similar to what SIA or Sembcorp Marine did.

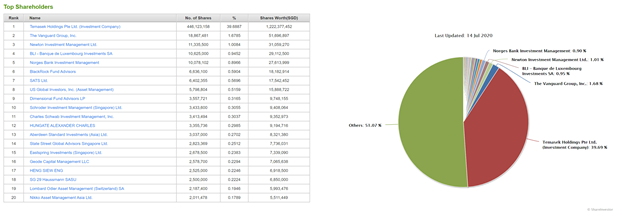

Temasek is a major shareholder with 39%, so it’s not hard to see them doing something similar here.

Source: ShareInvestor WebPro

Valuations

Valuations are super tough because we have no earnings visibility.

I came across 2 bank reports though, that contrast each other really well.

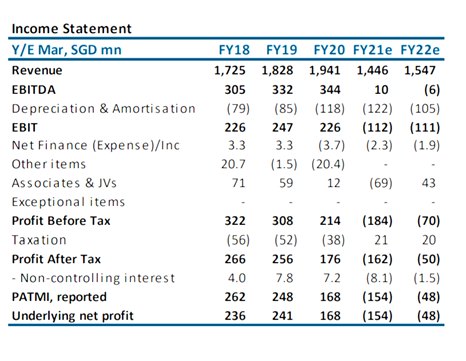

First, we have DBS, with a price target of $2.83.

They use a discounted cash flow analysis, and assume:

- A mild recovery from April 2021 – driven by cargo and non-aviation food

- PE pegged to 25x FY22 PE

- 0% weighted average cost of capital (WACC)

- 3% terminal growth (TG) assumptions

And then we have Phillips capital, which is uber bearish to the point where it’s funny.

They have a price target of $1.95, which is a 40% drop from here.

They’re basically assuming:

- No recovery until April 2022 at least

- Valuation of 1.35x book value being the 2009 trough

My personal view, is that Phillips Capital is too bearish, and DBS is too bullish.

I see the truth as falling somewhere in between. Which would give us a fair price of about $2.4?

Insider buys

Couple more points to look at then I’ll share my overall thoughts.

Insider buys are set out below.

Source: ShareInvestor WebPro

I use Shareinvestor to pull this data, which is more convenient than the alternative (trawling through SGX announcements). You can check out my review on ShareInvestor Webpro here.

Some minor insider buys, but nothing really notable to take note of.

If management were truly bullish on their own stock at this price, I would really like to see them put money where their mouth is. We need more of this in Singapore – real alignment of interests with shareholders.

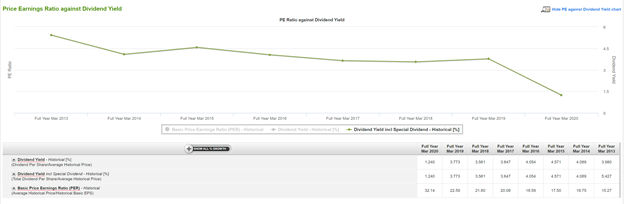

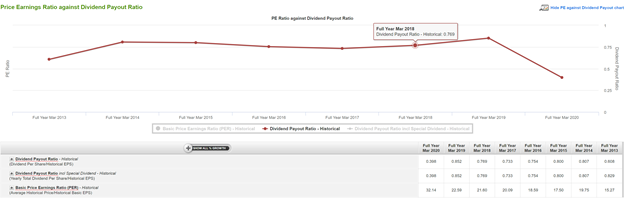

Dividend

In the good ol days, dividend yield is about 4% at a 75%+ payout ratio.

But let’s not kid ourselves right. There’s no more dividend for the next few years at least. The aviation industry is just in that bad a shape right now.

Source: ShareInvestor WebPro

Is SATS a good investment?

As much as I am an optimistic horse by nature, frankly I find it hard to be bullish on SATS.

The outlook is really bad.

Next quarter or two, I don’t see air travel recovering meaningfully.

Sure, if there’s positive vaccine news, this stock may spike a little, so that could be a trading opportunity.

But from an earnings perspective, it genuinely doesn’t look so good.

I also think there is a possibility of additional fund raising along the lines of what SIA and Sembcorp are doing, so definitely watch out for that if you are investing.

Management will try to diversify income away from aviation, but it’s tough to see that really replacing the hole from aviation.

I suspect international airtravel will gradually recover starting in 2021, but will probably not hit pre-COVID levels at least until 2023.

At some point, the government wage support will also start to fall off, which will really hit the bottom line.

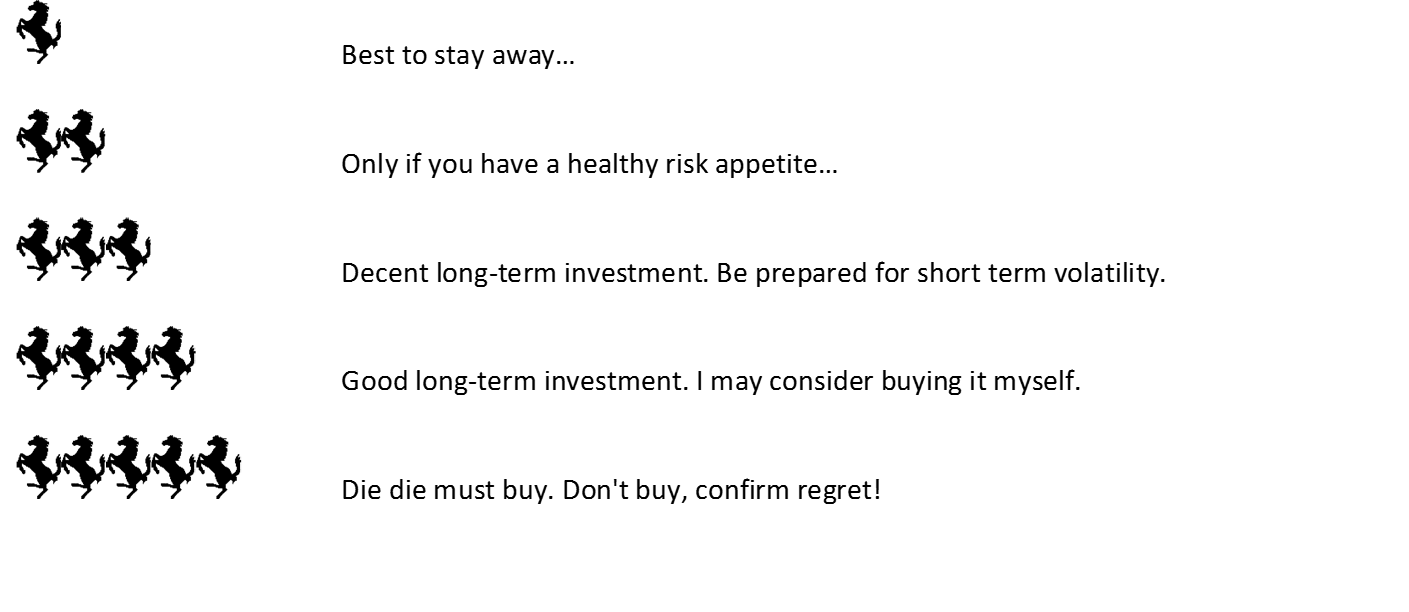

Closing Thoughts: 1.5 horses for me

I’ll give SATS a 1.5 horse rating (out of 5).

The stock has fallen almost 50% from highs, so there is a decent margin of safety. It’s just not enough in my view, given the uncertainties in play here.

There are just so many other great investing opportunities out there at the moment (my full stock watch is here), than for me to take a punt on an aviation services player right now.

The money could just sit there as dead money for extended periods, without significant potential for upside near term.

Throw in the risk of further downside, or capital calls, and the risk-reward just looks poor.

At some point in the future, SATS will be a good buy again. I have no doubt that eventually, air travel will recover.

But some things cannot be rushed. I need to let the short term fundraisings, earnings destruction etc play out naturally before I enter the stock.

Buying this stock now, for me, will be simply taking a blind bet that international aviation will recover, sooner rather than later. And making blind bets like that are not in my nature, nor are they a good way to invest in the longer term.

Do note that this article is written as at 31 July 2020, and will not be updated going forward. My latest thoughts, Stock Watch, and investment portfolio can be accessed on Patron.

SATS – Financial Horse Rating

![]()

Financial Horse rating scale

Share your comments below!

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

The post SATS: Why I will not invest in this stock appeared first on TinySG.

from TinySG https://tinysg.com/sats-why-i-will-not-invest-in-this-stock/?utm_source=rss&utm_medium=rss&utm_campaign=sats-why-i-will-not-invest-in-this-stock

No comments:

Post a Comment